There is a well-documented marketing principle that plays out every time an industry contracts: brands that maintain presence while competitors pull back tend to own a disproportionate share of the recovery. The financial services data from the past 12 months is a live case study of that principle in motion.

The market is quieter than it looks

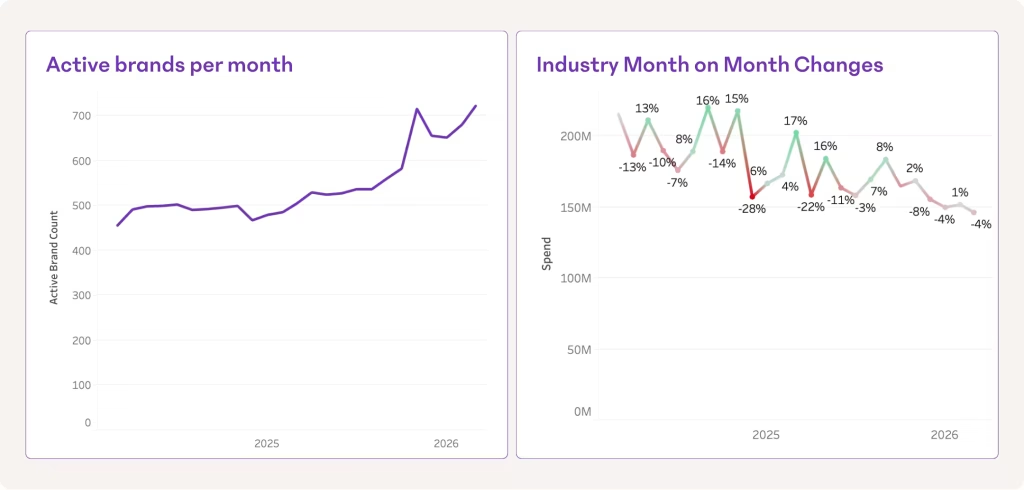

Total industry media spend in banking and finance is declining, while the number of brands advertising is rising. More brands are active, but each is advertising less. The result is a category that feels crowded but sounds quieter than before.

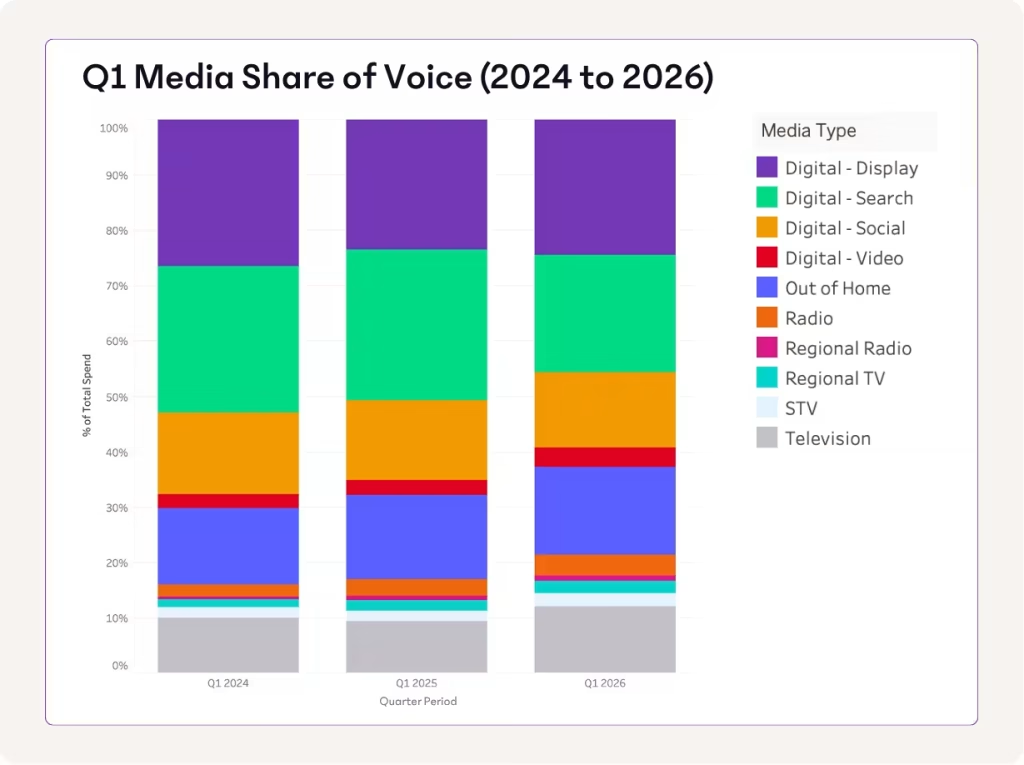

Digital channels tell the sharpest version of this story. Display, Search and Social are all materially down, averaging around -42% on a 12-month rolling basis. More telling: the Q4 seasonal surge in digital activity that has historically driven a late-year spike did not return in 2025. When competitors reduce their advertising budgets, the brands that don’t cut theirs get a larger share of audience attention—without necessarily spending more.

Offline has partially absorbed the reallocation, with TV, Radio and Regional TV each up 4–5% year-on-year. But OOH is down around 6%, and subscription TV has contracted by closer to 15%. The channel reallocation is real, but it isn’t tidy.

New entrants are reading the same signal

Over 50 brands made their lending debut in Q1 2026—brands with zero prior spend across Personal, Business or Home Loan categories in the two years before. Fifty new competitors moved into the same market in just three months. The gap established banks left didn’t stay empty for long.

Our brand-level forecasts show where this gap is widening. Incumbents still spending at scale are doing so across TV, radio, digital and out of home—but the majority are holding flat or pulling back across those channels. New entrants are not matching that scale, nor do they need to. They need only to be present where incumbents have gone quiet.

ANZ’s forecast is the most directional signal in the category, a major player betting that attention is about to become more valuable, not less. The increase doesn’t return spend to its prior peaks, but it doesn’t need to. It only needs to be louder than a quieter market.

The category is not recovering to its previous level. It is stabilising at a lower one.

For new entrants like CMC Invest and NRMA’s Home Loan arm, that distinction matters: the incumbents are not returning in full force. The space created by contracting budgets is not about to close as quickly as it opened.

Where the opportunity is largest

The window is open across the category, but it rewards different plays in different places.

Lending sub-categories are crowded: Home Loans, Business Banking and Personal Loans have absorbed the majority of new entrants, meaning visibility in these categories requires consistent, sustained presence.

Other sub-categories (Travel Cards, Debit Cards, Term Deposits) are dominated by fewer, larger advertisers, where the barriers to being heard are higher but so is the reward for breaking through.

For brands in lending, the conditions are unusually favourable right now. Budgets are contracting, attention is available, and at least one major incumbent has already decided the window is worth moving through.

See which brands are moving and which are going quiet. Connect with us and gain access to the full report.

References

Bigdatr Australia, Media Value data.